Welcome, humans.

He actually did it. IDK if y’all have been following this, but Tesla approved Elon Musk’s WILD $1 trillion dollar pay package, where Elon must achieve 12 market-cap step increases, from $1.4T today to $2T and all the way up to $8.5T.

In addition to raising the value of the company, he must also achieve 12 operational milestones: 20M vehicles delivered, 10M active FSD subscribers, 1M Optimus bots, 1M robotaxis, and EBITDA up to $400B three separate times (oh, and, for the last two tranches, he’s gotta come up with a board-approved CEO succession plan).

During a fireside chat and Q&A after the vote, Elon made all sorts of predictions and theorizing, like how he called Optimus an “infinite money glitch” (then again, he also said “maybe there won’t even be money in the future”, so there’s that) that could solve global inequality, deliver precision healthcare better than any human, and even reduce the need for prisons if Optimus just follows you around and stops you from doing crime lol.

That last one’s honestly my favorite. Imagine C3PO meets Robo-cop. It’ll help you do all kinds of household chores, errands, even creative projects. Just don’t try to get him to help you rob a bank or he’ll knock you out harder than K-2SO in that one Andor scene (you know the one).

Here’s what happened in AI today:

- We break down OpenAI’s “backstop gate” and the market jitters.

- Open Chinese model Kimi K2 Thinking beat GPT-5 at 6× lower cost.

- Google discussed investing in Anthropic at $350B+ valuation.

- October 2025 saw 153K+ AI-related job cuts, highest in two decades.

The TL;DR of OpenAI’s “Backstopgate” Saga, and the backdrop to the backstop (aka Kimi K2).

We promise that’ll all make sense if you read our deep dive below!

You know when you're talking in front of a crowd and can't find the right words? Well, when you're the CFO of OpenAI and those filler words get recorded at a WSJ event during a rough week for markets, things get spicy.

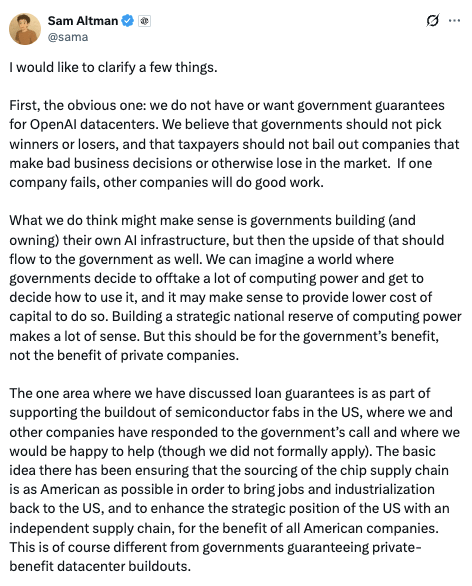

Hence the damage control tweet from @Sama:

Here's what happened to set this off: The Wall Street Journal ran a headline saying OpenAI CFO Sarah Friar wanted a federal backstop for AI investments. Uhhhh why do you want that if everything’s going well?? Cue the panic.

But it wasn't just her comments—it was a perfect storm of three things:

- First, Sam Altman had told economist Tyler Cowen that for sufficiently huge risks, "the government ends up as the insurer of last resort" (like nuclear power, not bailouts). When the WSJ headline dropped, it looked like OpenAI was asking to become "too big to fail."

- Second, Nvidia CEO Jensen Huang said China would win the AI race thanks to cheap power—then immediately walked it back. Even his clarification admitted China's "nanoseconds behind America."

- Third, Michael Burry (yes, The Big Short guy) disclosed massive puts on NVIDIA and Palantir. The Economist estimated an AI crash could wipe out ~$14.1 trillion in U.S. household wealth.

And what set all of this off to begin with? Sam’s flippant comments how if you don’t like our $1.4 trillion dollar deals, I’ll find someone to buy your shares.

Add that to all the usual macro factors, and markets panicked. Bitcoin dropped below $100K for the first time since June. The Fear & Greed Index hit 24 (Extreme Fear).

Our take: Where’s the lie with any of this? The biggest WTF moment was Jensen saying China “will” win the AI race.

At first we were confused, but then China dropped Kimi K2 Thinking—a 1-trillion parameter open model that scored 51% on Humanity's Last Exam, beating GPT-5, at 6× lower cost than Claude. Suddenly Jensen's original comment looked pretty spot on…

[Read the full story (w/ links to all the stuff mentioned) on the website here →]

FROM OUR PARTNERS

How to run a billboard campaign 101

You’re a fast-growing company ready to scale. You’re thinking big: billboards, airport ads, subway takeovers, all the stuff people can’t scroll past.

Delve just dropped the ultimate guide on how to plan, build, and launch an out-of-home campaign that drives quantifiable pipeline.

Learn the exact tactics we used to take over San Francisco, New York, and Texas with our viral “Done in Delve” campaign.

Whether you’re a scrappy startup trying to punch above your weight or a Series B company ready to make noise, this is your playbook for unforgettable brand moments.

Prompt Tip of the Day

Know what you want online, but not where to find it? One of the most efficient ways to get the exact url you’re looking for is to tell ChatGPT 5 Thinking (and ChatGPT specifically, because it has the widest access to the internet) the following:

“Can you give me the direct url for [ what you need here ].” |

I can’t tell you how often I realize I’m wasting time scouring Google search trying to get a specific link I know exists, but can’t remember how to find, and then I choose to ask ChatGPT for the “direct url”, and it delivers.

This is best for commercial links as opposed to more obscure ones, but I bet with that direct URL framing and enough context, you can direct OpenAI to give you nearly any url you’re looking for.

P.S: this also works if you ask for “publicly available contact information” for companies or individuals. Remember to specify “publicly available” because it’s against OpenAi’s terms to try and access any private information about other people.

Treats to Try

*Asterisk = from our partners (only the first one!). Advertise to 600K daily readers here!

- *Wispr Flow turns your speech into clean, final-draft writing across email, Slack, and docs. No start-stop fixing, no reformatting, just thought-to-text that keeps pace with you. Give your hands a break ➜ start flowing for free today.

- NotebookLM got yet another update: now you can create flashcards to memorize key terms from your uploaded documents, generate quizzes to test yourself, and temporarily toggle sources on/off so your AI assistant only references the specific files you want for each task.

- Gemini Deep Research now connects to Gmail, Drive, Docs, and Chat to combine live web research with your internal documents in one report.

- Manus 1.5 is a new general agent that builds full-stack web applications through conversation—you describe what you want, and it creates production-ready apps with databases, authentication, and embedded AI features like chatbots or image generation, plus it now has unlimited context and team collaboration features.

- Inception Labs released an upgraded version of Mercury, its flagship model that delivers higher quality than Claude 4.5 Haiku at one-fifth the latency and less than one-quarter the price ($0.25 per 1M input tokens, $1.00 per 1M output tokens)—making it fast enough for real-time autocomplete, voice agents, and in-the-flow coding assistants—try it here.

- And btw, the most impressive model demo we've seen in the last 12 months was how fast Mercury's diffusion based model (generating text like image models generate images) can generate working code.

- Harmonic AI is building a “Claude Code for math” via its Aristotle model that achieved gold-medal level performance at the 2025 International Mathematical Olympiad and now offers an API that completes formal math proofs in Lean4.

- Metropolis uses cameras to recognize your car or face so you can drive through parking garages, hotels, gas stations, and stores without stopping to pay or check in to, and now its scaling its camera-based recognition system across parking, retail, and gas stations (raised $1.6 billion; big business!).

- SemiAnalysis’ ClusterMAX 2.0 rates GPU cloud providers across 10 criteria (security, networking, reliability, monitoring, etc.) so you can compare 84 providers and find the best cluster for training models or running inference, with CoreWeave taking the top Platinum spot. (40K word report, video summary).

- Google launched File Search Tool in the Gemini API, a fully managed RAG (Retrieval Augmented Generation) system that automatically handles file storage, chunking, embeddings, and retrieval; it offers free storage (1GB free tier, up to 1TB in paid tiers) and free query-time embedding generation, with developers only paying $0.15 per 1M tokens for initial file indexing (Simon Willson said this code snippet is helpful for understanding what it can do).

- OlmoEarth analyzes satellite imagery to answer critical environmental questions—like tracking deforestation causes, identifying at-risk crops, or mapping wildfire risk—without needing complex data pipelines or specialized infrastructure—try it here

Around the Horn

- Google discussed deepening its investment in Anthropic, potentially valuing the AI startup above $350B after Anthropic's models outperformed rivals in key benchmarks.

- Microsoft faces Australian legal action for hiding cheaper non-AI subscription options from 2.7M customers, with regulators pursuing penalties up to $50M per breach.

- Microsoft research built a synthetic marketplace to test AI agents, revealing how even advanced models like GPT-4o struggle with basic real-world tasks and get easily manipulated.

- This breakthrough in brain-to-image technology achieved state-of-the-art fMRI image reconstruction using just 1 hour of brain data instead of the previously required 40 hours.

- David Baker's lab used AI to design antibodies from scratch that precisely target specified disease proteins.

- Bloomberg says October 2025 saw the highest monthly job cuts in two decades with “AI-driven layoffs” (or AI-blamed layoffs, lets say) affecting 153K+ positions—a shocking 183% increase from September.

FROM OUR PARTNERS

Adobe Firefly, Your Creative AI Studio

Adobe Firefly is an all-in-one creative AI studio that combines the industry’s top AI models from Adobe, Google, OpenAI, Runway, Luma AI, and more, with world-class tools for video, audio, imaging, and design. It’s everything you need to move ideas seamlessly from inspiration to finished content. One place. One plan. Built for speed, quality, and creative possibilities.

Through December 1, Adobe plan subscribers can enjoy unlimited image generations in the Firefly app. Experience the full power of creative AI today.

Intelligent Insights

- Peter H. Diamandis wrote about post-capitalism, and what happens in a world of abundant energy, education, and food (TL;DR = we won’t need money, so intangible experiences will be the scarcest resource; in our opinion we’re a long way from that reality due to AI’s current limitations, but it shows the possibility of what a world with self-improving AI that make more and more efficient resources for us looks like. This is why we still need new breakthroughs!)

- Alberto Roberto wrote about the two biggest conflicting studies in AI (MIT’s report on how 95% of gen-ai pilots fail, and Wharton’s report about how 75% of enterprises see positive ROI on genAI), and that you can’t really trust either of them (and better yet, why not).

- Arnon Shimoni writes that AI-generated content is creating a "trust collapse" online, where despite improving technical quality, AI material feels increasingly soulless and unreliable, which makes marketing all about gaining trust.

- Devansh’s breakdown of “AI Slop” explains why the internet became saturated with machine-generated content, revealing how platforms profit twice—first by allowing pollution, then by charging for filters to find authentic information.

- Ben Thomson of Stratechery writes why tech bubbles like the current AI boom aren't just irrational exuberance but actually function as critical coordination mechanisms that drive infrastructure development with benefits “literally forever.”

A Cat’s Commentary